JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the fourth quarter and year ended 31 December 2022.

This update provides a summary of recent developments in the uranium and nuclear industries, as well as provisional information related to the Company’s key fourth-quarter and 2022 operating and trading results, and non-financial 2023 guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

In November 2022 countries gathered at the Sharm el-Sheikh Climate Change Conference (COP 27) to take action toward meeting global climate goals set forth in the Paris Agreement. COP 27 ended with a draft agreement that highlights the crucial role of multilateralism in addressing climate change and reiterates the conclusions of all prior COP meetings. It is also worth noting that the agreement calls for an “increase in low emission and renewable energy” as part of “diversifying energy mixes and systems”. Incorporation of technology-inclusive wording in its call for the decarbonisation of the world energy system expands the opportunities for all low-carbon generating sources, including nuclear power.

In an effort to transition away from coal-fired generation and boost its level of energy independence, the Polish government has chosen to collaborate with the American government and Westinghouse Electric Co. (Westinghouse) to construct the country's first nuclear power plant. According to the agreement, Westinghouse will provide three AP1000 PWRs for the initial phase of the Polish Nuclear Power Program. With a goal of constructing between 6 and 9 GWe in total capacity by the early 2040s, Poland plans to commence initial criticality on its first reactor, which Westinghouse will supply, as early as 2033. According to the Polish government, the first three-unit nuclear power plant in Poland will be located at the coastal community of Choczewo at the Lubiatowo-Kopalino location close to the Baltic Sea.

The Dutch government has confirmed plans to build two large reactors at the existing Borssele nuclear power plant by 2035. The two third-generation reactors will each have a capacity of 1,000 MWe to 1,650 MWe. The country chose nuclear energy because the Netherlands requires all clean energy sources to meet climate goals and reach zero carbon emissions in electricity production by 2040 at the latest. In addition, the government announced plans to extend the operating life of the single-unit Borssele nuclear power plant beyond its current license expiration date of 2033.

The UK Department of Business, Energy and Industrial Strategy announced plans to provide £77 million in government funding to support nuclear fuel production and advanced reactor development. Westinghouse has already been awarded £13 million to investigate the potential development of conversion capabilities at its Springfields site in Lancashire, England. The UK's Advanced Modular Reactor R&D program will be provided £60 million in funding to support high temperature gas reactor (HTGR) research, which is expected to be operational in the early 2030s.

German lawmakers agreed to postpone the planned shutdown of the country's last three nuclear power plants in 2022 until mid-April 2023 in response to concerns about winter electricity shortages in Germany. The Atomic Energy Law of the country establishes a legal framework for the extension of the nuclear power plants Isar unit 2, Neckarwestheim unit 2, and Emsland. The German’s government's latest decision to keep the units operational past their scheduled shutdown date of 31 December 2022 is seen as a compromise between the anti-nuclear German Greens and the pro-business Free Democratic Party that would prefer to keep the country's remaining reactors operational until 2024.

Late December 2022, Government of Japan approved a plan to revive the use of nuclear energy. Under a new policy, the country announced it would “maximize the use of existing nuclear reactors” by accelerating restarts in a reversal of a post-Fukushima plan to phase out use of nuclear power plants. Additionally, an intend to extend of lifespan of nuclear reactors beyond 60 years was announced, as well as plans to develop advanced reactors to replace decommissioned ones.

Beyond policy highlights, a number of new demand announcements took place during the fourth quarter:

- Rosatom announced the official start of construction for El Dabaa unit 2 in Egypt. El Dabaa unit 2 is the second of four VVER-1200 reactors designed by Russia to be built at the El Dabaa site on Egypt's northern Mediterranean coast.

- Hungary's parliament approved plans to extend the life of the four operating VVER-440 reactors at the Paks nuclear power plant in central Hungary. With the government's approval, the state can begin preparing to operate the Paks nuclear power plant for an additional 20 years.

- In a similar development, at the very beginning of 2023, subsequent to the end of the quarter, the French energy company ENGIE and the Belgian government have agreed to extend the service life of Doel unit 4 and Tihange unit 3 by ten years each to 2035.

- China National Nuclear Corp. (CNNC) announced the beginning of the construction phase of CAP-1000 PWR at Haiyang unit 4 in Shandong Province, China, which is a project owned and operated by State Power Investment Corp. (SPIC).

- Subsequent to the quarter end, China General Nuclear (CGN) announced that Fangchenggang unit 3 in China's Guangxi Autonomous Region has been connected to the grid for the first time. The 1,180 MWe PWR was synchronised with the grid on January 10, and is scheduled to go commercial in the second half of 2023.

Several “unconventional demand” developments emerged during the fourth quarter:

- In December, US Department of Energy’s National Nuclear Security Administration (NNSA) awarded contracts for 1.1 million pounds U3O8 under the US Uranium Reserve program to five U.S. uranium producers: enCore Energy, Energy Fuels, Peninsula Energy, Ur-Energy and Uranium Energy Corp. These awards are part of the initial US$ 75 million authorized by US Congress in 2020 to advance the US Government’s goal of supporting the US nuclear fuel supply chain and capabilities. In addition to the awards to uranium producers, NNSA has awarded a five-year, sole source contract valued at US$ 14.5 million contract to ConverDyn to convert U3O8 into uranium hexafluoride (UF6).

- The Alashankou Natural Uranium Bonded Warehouse on China's eastern border with Kazakhstan has received its first delivery of natural uranium for storage. The warehouse, which is being constructed in three phases, aspires to become a major uranium trading hub in the coming years. Phase I, capable of holding up to 3,000 tU (7.8 million pounds U3O8) has been successfully completed at the end of 2021, and construction of Phase II with an additional capacity of 10,000 tU (26 million pounds U3O8) is currently underway.

On the supply side, Cameco Corp. (Cameco) announced on November 9, 2022 that the first pounds of uranium ore from the McArthur River mine had been milled and packaged at the Key Lake mill, marking the achievement of initial production as these facilities resume normal operations after being placed on care and maintenance in January 2018. Cameco intends to produce 15 million pounds U3O8 (100% basis) per year from these operations beginning in 2024, which is 40% less than their annual licensed capacity, as part of its ongoing strategy to align production decisions with customer procurement needs.

Finally, in another notable highlight, Cameco and Brookfield Renewable Partners announced a strategic partnership to acquire Westinghouse for approximately US$7.9 billion. Brookfield Renewable will own 51% of Westinghouse after the transaction, which is expected to close in the second half of 2023, with Cameco owning the remaining 49%. Cameco stated that Westinghouse 's existing debt structure will remain in place, leaving the consortium with an estimated US$4.5 billion equity cost, subject to closing adjustments. This equity cost will be shared proportionately between Brookfield and its institutional partners (~US$ 2.3 billion) and Cameco (~US$ 2.2 billion).

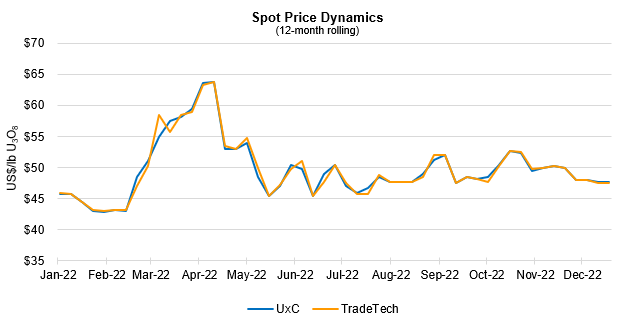

Market Pricing and Activity

Spot market activity picked up in October with increased buyers’ interest, pushing spot price to US$52.68/lb U3O8. With utilities largely missing, buyers included traders, financials, and producers. In November, the spot market activity slowed down slightly, with spot price hovering around US$50.00/lb U3O8 throughout the month. As the holiday season got underway, spot activity decreased even further, with the spot price declining to about US$47.68/lb U3O8 by the end of the year. According to third-party market data, spot volumes transacted through 2022 were almost 50% lower than the last year. A total of approximately 52 million pounds U3O8 (20,000 tU) was transacted at an average weekly spot price of US$49.61/lb U3O8, compared to about 99 million pounds U3O8 (38,000 tU) at an average weekly spot price of US$35.05/lb U3O8 during 2021.

In the term market, third-party data indicated that contracted volumes totaled about 114 million pounds U3O8 (43,800 tU) through 2022, compared to about 72 million pounds U3O8 (27,700 tU) in 2021. The 60% increase in term contracting activity in 2022, led to a notable US$9.25/lb U3O8 increase of the long-term price indicator year-over-year, resulting in an average term price of US$52.00/lb U3O8 (reported on monthly basis by third-party sources).

Company Developments

Transportation risk mitigation

As was previously disclosed, Kazatomprom has completed a physical delivery of natural uranium using the Trans-Caspian International Transport Route (TITR) in December 2022. The Company has successfully used the TITR as an alternative route for delivering Kazatomprom’s material to western customers since 2018, helping to mitigate the risk of the primary route through St. Petersburg being unavailable, for any reason.

Kazatomprom continues to monitor the growing list of sanctions on Russia and the potential impact they could have on the transportation of products through Russian territory. To date, there are no restrictions on the Company's activities related to the supply of its products to customers worldwide.

Management Changes

As was disclosed in December, 2022, Mrs. Kamila Syzdykova, Kazatomprom’s Chief Financial Officer (“CFO”), and Mr. Askar Batyrbayev, Kazatomprom’s Chief Commercial Officer (“CCO”), have decided to leave their roles at the Company to pursue other opportunities effective 04 January 2023 and 11 January 2023 respectively.

Ruslan Beketayev, who has previously served as Deputy Chairman of the Board at the Eurasian Development Bank and before that held the position of the Vice Minister of the Ministry of Finance of the Republic of Kazakhstan, was appointed as CFO effective 11 January 2023.

Alisher Taizhanov, former Director of Kazatomprom’s Sales Support Department, who has been with the Company’s Group since 2014, was appointed as CCO effective 11 January 2023 and as a member of the Executive Board, effective 12 January 2023 respectively.

Kazatomprom’s senior management team currently consists of:

- Yerzhan Mukanov, Chief Executive Officer and Chairman of the Executive Board;

- Alisher Taizhanov, Chief Commercial Officer, member of the Executive Board;

- Dosbolat Sarymsakov, Chief Nuclear Fuel Cycle Officer, member of the Executive Board;

- Alibek Aldongarov, Chief HR and Digitalisation Officer, member of the Executive Board;

- Ruslan Beketayev, Chief Financial Officer;

- Marat Yelemessov, Managing Director of Legal Support and Risks, Member of the Executive Board (currently on academic leave).

Full biographies of the Executive Board are available on the Company’s website: https://www.kazatomprom.kz

First delivery of nuclear fuel from Kazakhstan

In December 2022, Ulba-FA LLP fuel assembly fabrication plant (the Plant), which began the commercial operation in 2021, carried out the first delivery of nuclear fuel for one reload (a little over 30 tons of low-enriched uranium) to China, where the product was accepted by a Chinese corporation China General Nuclear Power Corporation-Uranium Resources Co. («CGNPC-URC»). Further, the Plant plans to increase the production volumes to reach the full annual production capacity of 200 tons of uranium in the form of fuel assemblies in 2024.

Placement and redemption of Short-term Bonds

As was disclosed in the interim consolidated financial statements for the three and nine month periods ended 30 September 2022, Kazatomprom’s Board of Directors on 27 October 2022 approved four issues of the Company's commercial bonds totalling 200,000,000 (two hundred million) US Dollars. The issue and placement of bonds will be carried out according to the Company’s short-term liquidity needs. The placement of the Company’s first issue of bonds (ISIN KZ2C00009199) in the "Debt Securities" sector of the "Main" platform of JSC "Kazakhstan Stock Exchange" ("KASE") in the "Commercial Bonds" category took place on December 23, 2022.

The placement of the first issue of commercial bonds is made under the following conditions:

- Type of bonds (being issued): unsecured coupon commercial bonds

- Total volume of the bond issue: 50,000,000 (fifty million) US Dollars

- Number of bonds: 500,000 (five hundred thousand) pieces

- Maturity date: 30 (thirty) calendar days from the issue date

- Nominal value of one bond and the currency of the nominal value: 100 (one hundred) US Dollars

- Interest rate (coupon): 4.32% (determined as the Secured Overnight Financing Rate (SOFR) published on the official website of the Federal Reserve Bank of New York: (https://www.newyorkfed.org/markets/referencerates/sofr) as of 15 December 2022)

- Yield to maturity: 4.60%

- Clean price: 99.9768%

- Total placement amount: 49,988,400 (forty-nine million nine-hundred and eighty-eight thousand and four hundred) US Dollars

On 23 January 2023, the bond issue was redeemed. Total payments for the issue amounted to US$ 50,180,000 (fifty million and one hundred and eighty thousand), including:

- Principal debt (nominal bond value) – 50,000,000 (fifty million) US Dollars

- Coupon payment – 180,000 (one hundred and eighty thousand) US Dollars. Coupon payment for 30 calendar days amounted to 36 US cents per one bond.

Credit Rating

On December 15 2022, Fitch Ratings reaffirmed Kazatomprom’s credit rating at BBB-, Outlook – Stable. On December 28 2022, Moody’s Investors Service reaffirmed Kazatomprom’s credit rating at Baa2, Outlook – Stable.

ESG Rating

As was disclosed in December 2022, S&P Global Ratings assigned the Company an Environmental, Social and Governance (ESG) Evaluation score of 51/100. Kazatomprom's ESG Evaluation score is based on the rating agency’s view of the Company’s relative exposure to observable ESG-related risks and opportunities, and its qualitative opinion of the Company’s long-term sustainability and readiness for emerging trends and potential disruptions. The Company’s current ESG Evaluation score of 51 reflects the mining industry's significant exposure to inherent environmental and social risks, which are partly offset by the Company's effective ESG management practices, primarily related to the highly regulated nature of its businesses at both the local and international levels. Of note, the current global maximum ESG evaluation score among Metal & Mining sector companies is 68 (of 100) with a global Metals & Mining sector average of 50 (out of 100).

Kazatomprom’s 2022 Fourth-Quarter Operational Results1

|

|

Three months ended December 31 |

|

Year ended December 31 |

|

||

|

(tU as U3O8 unless noted) |

2022 |

2021 |

Change |

2022 |

2021 |

Change |

|

Production volume (100% basis)2 |

5,780 |

5,860 |

-1% |

21,227 |

21,819 |

-3% |

|

Production volume (attributable basis)3 |

3,064 |

3,066 |

0% |

11,373 |

11,858 |

-4% |

|

Group sales volume (consolidated)4 |

3,025 |

8,117 |

-63% |

16,358 |

16,526 |

-1% |

|

KAP sales volume (incl. in Group)5 |

1,340 |

6,788 |

-80% |

13,572 |

13,586 |

0% |

|

Group average realised price (USD/lb U3O8)6* |

47.51 |

35.82 |

33% |

43.46 |

33.11 |

31% |

|

KAP average realised price (USD/lb U3O8)7* |

48.61 |

34.45 |

41% |

42.51 |

32.33 |

31% |

|

Average month-end spot price (USD/lb U3O8)8* |

49.94 |

44.33 |

13% |

49.81 |

35.28 |

41% |

1 All values are preliminary.

2 U3O8 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it therefore disregards the fact that some portion of that production may be attributable to the Group’s joint venture partners or other third- party shareholders. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 U3O8 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, which corresponds only to the size of such interest; it therefore excludes the remaining portion attributable to the JV partners or other third-party shareholders, except for production from JV “Inkai” LLP, where the annual share of production is determined as per the Implementation Agreement disclosed in the IPO Prospectus. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

4 Group U3O8 sales volume: includes the sales of U3O8 by Kazatomprom and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity). Group U3O8 sales volumes do not include other forms of uranium products (including, but not limited to, the sales of fuel pellets).

5 KAP U3O8 sales volume (incl. in Group): includes only the total external sales of U3O8 of KAP and Trade House KazakAtom AG (THK). Intercompany transactions between KAP and THK are not included. Volume does not include approximately 32 tU equivalent sold as UF6 in 2Q22 and 225 tU equivalent sold as UF6 in 4Q21.

6 Group average realised price (USD/lb U3O8): average includes Kazatomprom’s sales and those of its consolidated subsidiaries, as defined in footnote 4 above.

7 KAP average realised price (USD/lb U3O8): the weighted average price per pound for the total external sales of KAP and THK. The pricing of intercompany transactions between KAP and THK are not included.

8 Source: UxC LLC, TradeTech. Values provided are the average of the month-end uranium spot prices quoted by UxC and TradeTech, and not the average of each weekly quoted spot price throughout the month. Contract price terms generally reference month-end prices.

* Note the conversion of kgU to pounds U3O8 is 2.5998.

Production volumes on a 100% basis and attributable basis for both fourth quarter of 2022 and throughout 2022 were slightly lower compared to 2021. COVID-19 pandemic had an impact on wellfield development in 2021. This had a lagged effect on the production, as it usually takes from eight to ten months between wellfield development and the resulting uranium extraction by in-situ recovery. Therefore, and given that COVID-19 has also affected delays and/or limited access to certain materials and equipment, resulted in lower production in 2022 compared to the same period in 2021. Additionally, attributable production was impacted by the sale of a 49% share of “Ortalyk” LLP to CGN Mining UK Limited in July 2021.

Uranium sales at the Group and KAP levels in 2022 were on the same level as in 2021. Due to the timing of customer requirements and differences in the timing of deliveries, significantly lower proportion of both Group and KAP sales occurred in the fourth quarter, compared to the same period in 2021. Shipment through TITR that included the JV Inkai-owned portion of the material was successfully delivered, accordingly the Group sales volume stayed within the forecast range for 2022.

Average realised prices for the Group and KAP in the fourth quarter and for the full year of 2022 were higher compared to the same periods in 2021 due to the higher spot price of uranium. The Company’s current overall contract portfolio pricing correlates to uranium spot prices. However, for short-term deliveries to end-user utilities, the spot price can vary between the time contract pricing is established according to Kazakh transfer pricing regulations, and the spot price in the general market when the actual delivery takes place. The impact of market volatility during the time lag between price-setting and delivery becomes more pronounced as volatility increases, in both rising and falling price conditions. In addition, some long-term contracts incorporate a proportion of fixed pricing negotiated prior to the sharp increase in spot price in the second half of 2021. As a result, increases in both the Group and KAP’s average realised prices in 2022 compared to 2021 were lower than the increases in the spot market price for uranium over the same intervals.

Kazatomprom’s 2023 Production and Sales Guidance

|

(tU as U3O8 unless noted) |

|

|

2023 |

2022 |

|

Production volume U3O8 (100% basis)1 |

|

|

20,500 – 21,5002 |

21,000 – 22,000 |

|

Production volume U3O8 (attributable basis)3 |

|

|

10,600 – 11,2002 |

10,900 – 11,500 |

|

Group sales volume (consolidated)4, 5 |

|

|

15,400 – 15,900 |

16,300 – 16,800 |

|

Incl. KAP sales volume (incl. in Group)5 |

|

|

12,100 – 12,600 |

13,400 – 13,900 |

1 Production volume U3O8 (tU) (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it disregards that some portion of production may be attributable to the Group’s JV partners or other third-party shareholders.

2 The duration and full impact of the COVID-19 pandemic and the Russian-Ukrainian conflict are not yet known. Annual production volumes could therefore vary from expectations.

3 Production volume U3O8 (tU) (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, corresponding only to the size of such interest; it excludes the portion attributable to the JV partners or other third-party shareholders, except for JV “Inkai” LLP, where the annual share of production is determined as per Implementation Agreement disclosed in the IPO Prospectus.

4 Group sales volume: includes the sales of U3O8 by Kazatomprom and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity). Group U3O8 sales volumes do not include other forms of uranium products (including, but not limited to, the sales of fuel pellets).

5 KAP sales volume: includes only the total external sales of U3O8 of KAP and THK. Intercompany transactions between KAP and THK are not included.

* Please note that the conversion of kgU to pounds U3O8 is 2.5998.

Kazatomprom’s production expectations for 2023 remain consistent with its market-centric strategy and the intention to flex down planned production volumes by 20% for 2018 through 2023 (versus planned production levels under Subsoil Use Agreements). Production volume in 2023 is expected to be between 20,500 tU and 21,500 tU on a 100% basis and between 10,600 tU and 11,200 tU on an attributable basis. Decrease in production guidance for 2023 in comparison to 2022 is mainly due to continued delays and/or limited access to certain key materials, including sulfuric acid, and equipment impacting the wellfield commissioning schedule in 2022.

Sales volume guidance for 2023 is aligned with the Company’s market-centric strategy as well. The Group expects to sell between 15,400 tU and 15,900 tU, which includes KAP sales of between 12,100 tU and 12,600 tU. Decrease in U3O8 sales volume guidance for 2023 in comparison to 2022 both at the Group and KAP levels is due to the expected lower production and higher sales in forms other than U3O8, including but not limited to fuel pellets produced from KAP’s U3O8.

The Company continues to target an ongoing inventory level of approximately six to seven months of annual attributable production. The Company may purchase uranium from the spot market, while continuing to monitor market conditions for opportunities to optimise its inventory.

Wellfield development, procurement and supply chain issues, including inflationary pressure on production materials and reagents, are expected to continue throughout 2023, impacting the Company’s financial metrics. Changes to the tax code of the Republic of Kazakhstan on Mineral Extraction Tax, which came into effect in 2023, will have an additional impact on the Company’s financial performance. The expenditures related to the local social funding requests are possible as well. However, these risks cannot be quantified or estimated at this time. Financial guidance for 2023 will be published in the Operating and Financial Review for 2022, expected to be released on 14 March 2023.

Conference Call Notification – 2022 Operating and Financial Review (14 March 2023)

Kazatomprom expects to schedule a conference call to discuss the full 2022 operating and financial results, after they are released on Tuesday, 14 March 2023. Further details will be provided closer to the date of the event.

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Yerlan Magzumov, Director of Investor Relations

Tel: +7 7172 45 81 80

Email: ir![]() kazatomprom.kz

kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Sabina Kumurbekova, Director of the GR and PR Department

Gazhaiyp Kumisbek, Chief Expert of GR & PR Department

Tel.: +7 7172 45 80 22

Email: pr![]() kazatomprom.kz

kazatomprom.kz

Copy of this announcement will be available at https://www.kazatomprom.kz.

About Kazatomprom

Kazatomprom is the largest uranium producer in the world with natural uranium production in proportion to the Company's participatory interest in the amount of about 24% of the total global primary uranium production in 2021. The group has the largest uranium reserve base in the industry. Kazatomprom, together with subsidiaries, affiliates and joint organisations, is developing 26 deposits combined into 14 uranium-mining enterprises. All uranium mining enterprises are located on the territory of the Republic of Kazakhstan and when mine uranium use in-situ recovery technology, paying particular attention to best HSE practices and means (ISO 45001 and ISO 14001 certified).

Kazatomprom's securities are listed on the London Stock Exchange, the Astana International Exchange and the Kazakhstan Stock Exchange. Kazatomprom is the National Atomic Company of the Republic of Kazakhstan, and the main customers of the group are operators of nuclear generating capacities, and the main export markets for products are China, South and East Asia, North America and Europe. The Group sells uranium and uranium products under long-term and short-term contracts, as well as on the spot market directly from its corporate centre in Astana, Kazakhstan, as well as through a trading subsidiary in Switzerland, Trading House KazakAtom (THK).

For more information, please, visit our website https://www.kazatomprom.kz.

Statements for the Future

All statements, other than statements of historical fact, included in this message or document are statements regarding the future. Statements regarding the future reflect the Company's current expectations and estimates regarding its financial condition, results of operations, plans, goals, future results and activities. Such statements may include, but are not limited to, statements before which, after which or where words such as “goal”, “believe”, “expect”, “intend”, “possibly”, “anticipate”, “evaluate”, “plan”, “project”, “will”, “may”, “probably”, “should”, “may” and other words and terms of a similar meaning or their negative forms are used.

Such statements regarding the future include known and unknown risks, uncertainties and other important factors beyond the control of the Company, which may lead to the fact that the actual results, indicators or achievements of the Company will significantly differ from the expected results, indicators or achievements expressed or implied by such statements regarding the future. Such statements regarding the future are based on numerous assumptions regarding the current and future business strategy of the Company and the conditions in which it will operate in the future.

INFORMATION ON THE ESTIMATES CONTAINED IN THIS DOCUMENT ARE BASED ON SEVERAL ASSUMPTIONS ABOUT FUTURE EVENTS AND ARE SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTIES AND OTHER CONVENTIONALITIES, NONE OF WHICH CAN NOT BE PREDICTED WITH CERTAINTY AND SOME OF WHICH ARE OUTSIDE OF THE COMPANY'S CONTROL. THERE CAN NOT BE ANY WARRANTY THAT THE ESTIMATES WILL BE REALISED AND THE ACTUAL RESULTS MAY BE ABOVE OR BELOW THAN SPECIFIED. NONE OF THE COMPANY - NO SHAREHOLDERS, NO DIRECTORS, NO OFFICERS, NO EMPLOYEES, NO CONSULTANTS, NO AFFILIATES NOR ANY REPRESENTATIVES OR AFFILIATES LISTED ABOVE BEAR RESPONSIBILITY FOR THE ACCURACY OF THE ESTIMATES PRESENTED IN THIS DOCUMENT.

The information contained in this message or document, including, but not limited to, statements regarding the future, is applicable only as of the date of this document and is not intended to provide any guarantees regarding future results The Company expressly disclaims any obligation to disseminate updates or changes to such information, including financial data or forward-looking statements, and will not publicly release any changes that it may make to information arising from changes in the Company's expectations, changes in events, conditions or circumstances on which such statements regarding the future are based, or in other events or circumstances arising after the date of this document.